SBA Business Valuations for Business Owners

Your business is likely one of your most valuable assets and knowing its worth is critical to key life decisions including developing an exit or succession plan, preparing for acquisition & growth, gifting or estate planning, and dealing with divorce, or other significant events. An SBA business valuation is a critical tool to support your plans for growth or for future business transitions.

A crucial step in the process is selecting a business valuation firm staffed with accredited appraisers and the right experience. Our team of highly experienced appraisers and analysts oversees more than 2,000 business valuation engagements per year. We have seen it all. No business is too large or too small, too simple or too complex.

What is a business valuation?

A business valuation is a result of determining the monetary worth of a business, using objective metrics and other value identifiers. You may need one if your business is going through a change in ownership, a sale, or exit planning.

Take a look at our Additional Services

- Income Statement Adjustment (Add-Back)Tracing

- Working Capital Analysis

When would I need a business valuation?

Whether you are a small business owner or someone who serves small business owners, there will come a time when you’ll need to know the value of a business to guide key decisions.

Here are our top 8 scenarios in which you’ll need a valuation:

- SBA Lending

- Listing a Business for Sale

- Business Planning

- ESOP

- Gift Tax / Estate Tax

- Corporation Tax Filing Status

- Partner Buy-Outs / Disputes

- Marital Dissolution

For more information about why you may need an appraisal, read our blog.

When are Business Valuations Required for an SBA Loan?

SBA Lenders will require a business valuation for a change of ownership transaction if the amount being financed (minus the appraised value of the real estate and/or equipment) is greater than $250,000 and/or if there is a close relationship between the buyer and seller. In some cases, the lender will also require a business valuation when the subject company being sold has been under existing ownership for less than three years. In all cases, the lender must obtain an independent business valuation from a qualified source.

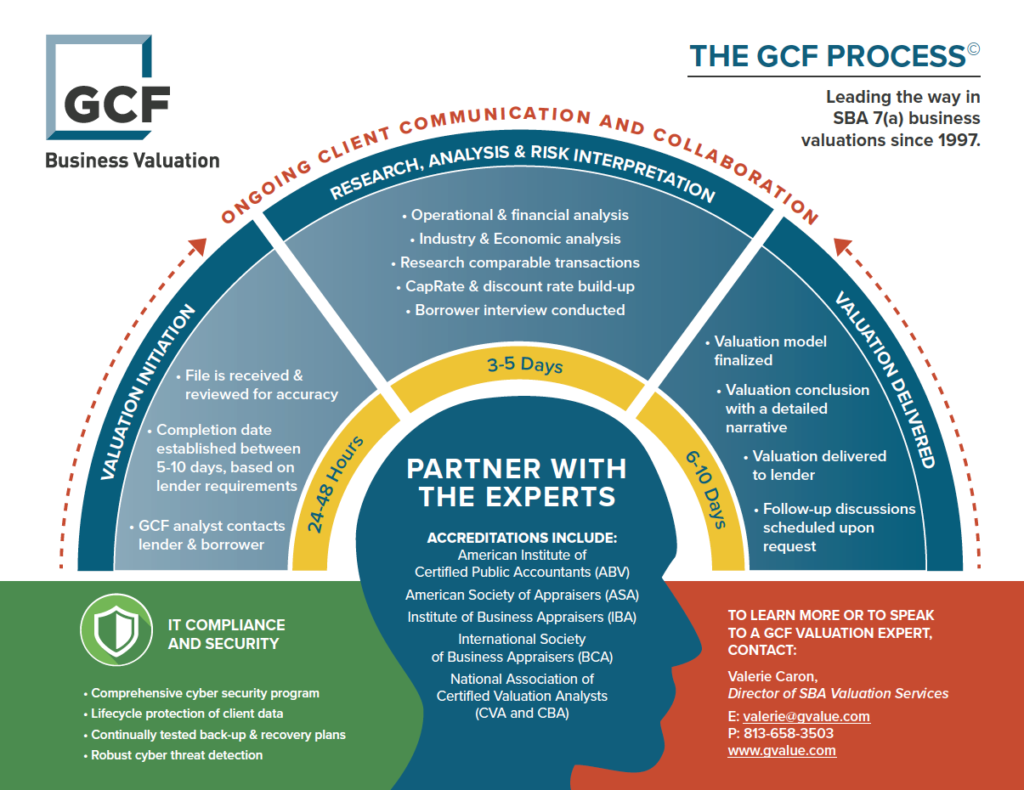

The Process of Obtaining an SBA-Compliant Business Valuation

- The SBA Lender Must Engage the Appraiser Directly: The appraiser must be qualified and experienced in SBA-compliant valuations. The appraiser must be accredited and knowledgeable about the specific requirements of SBA lending and business valuation (SBA SOP). The lender and the SBA are the sole intended users of the business valuation.

Each member of the GCF appraisal team holds one or more of the following accreditations: Accredited Senior Appraiser (ASA), Certified Business Appraiser (CBA), Certified Valuation Analyst (CVA), Accredited in Business Valuation by the American Institute of CPAs (ABV by AICPA), Accredited in Business Valuation (ABV). Learn more about GCF’s credibility and accreditations. - Provide Financial and Operational Information: The appraiser will need access to detailed financial records, including income statements, balance sheets, tax returns, and other relevant documents about the business’s operations. In addition, Industry, Economic, and Market Data, are also part of the appraiser’s analysis and considered part of the value conclusion.

- Analysis and Valuation: The appraiser will analyze all of the information gathered as part of the engagement and determine the conclusion of value using three approaches to value; Income Approach, Market Approach, and Cost Approach. The SBA requires the appraiser to use Fair Market Value as the basis of the conclusion.

- Receive the Valuation Report: Once the appraisal is complete, the appraiser will provide a final copy of the report to the lender, which will then be considered as part of the lender’s decision to approve the SBA Loan.

Tips for Preparing for an SBA-Compliant Business Valuation

- Organize Your Financial Records: Ensure your financial statements, tax returns, and other relevant financial documents are well-organized and current. This helps the lender and the appraiser conduct a more accurate and efficient analysis.

- Understand Your Business’s Market and Industry: Be prepared to provide your business’s position within its market and industry trends. This knowledge will aid the appraiser in assessing the business’s potential for growth and sustainability.

Gain insight into the value of your business and industry trends with GCF’s Market Intelligence Reports. View them here

- Maintain Transparency: Provide complete and accurate information to the lender (and appraiser). Any discrepancies or omissions can hinder the appraisal process and may raise concerns.

- Prepare for Questions: The appraiser may ask questions about the business’s operations, plans, and potential risks. Being prepared with thoughtful and honest answers will facilitate an efficient valuation process.

By understanding the significance of Business Valuations and preparing adequately, small business owners can facilitate a smooth loan approval process for all parties involved (SBA Lender, Borrower, Appraiser). This prevents any delays during loan underwriting, and more importantly, surprises just before closing.

Learn more about business valuations:

Download our free guide: How to Navigate the Business Valuation Process Successfully

Read: Why & When You Need a Business Valuation

Read: Different Types of Business Valuations

Start the Process

Are you ready to learn more about the value of your business? Contact us to get started.

SBA Business Valuation Accreditation

Your GCF Business Valuation appraisal team has one or more of the following accreditations:

Accredited Senior Appraiser (ASA) – is recognized as having achieved the highest level of education, training, and report writing for business valuations. The ASA designation is the gold standard for a business valuation professional. (source: American Society of Appraisers)

Accredited Senior Appraiser (ASA) – is recognized as having achieved the highest level of education, training, and report writing for business valuations. The ASA designation is the gold standard for a business valuation professional. (source: American Society of Appraisers) Certified Business Appraiser (CBA) – a very prestigious credential in the eyes of all who are familiar with it as it earned the reputation of being a difficult credential to obtain. (source: National Association of Certified Valuators and Analysts®)

Certified Business Appraiser (CBA) – a very prestigious credential in the eyes of all who are familiar with it as it earned the reputation of being a difficult credential to obtain. (source: National Association of Certified Valuators and Analysts®)

Certified Valuation Analyst (CVA)

Certified Valuation Analyst (CVA)

Accredited in Business Valuation by the American Institute of CPAs (ABV by AICPA) – a credential granted exclusively by the AICPA to qualified valuation professionals who demonstrate expertise in valuation through knowledge, skill, experience, and adherence to professional standards. (source: American Institute of CPAs)

Accredited in Business Valuation by the American Institute of CPAs (ABV by AICPA) – a credential granted exclusively by the AICPA to qualified valuation professionals who demonstrate expertise in valuation through knowledge, skill, experience, and adherence to professional standards. (source: American Institute of CPAs)- Accredited in Business Valuation (ABV) – credential is granted exclusively by the AICPA to CPAs and qualified valuation professionals who demonstrate considerable expertise in valuation through their knowledge, skill, experience, and adherence to professional standards. (source: American Institute of CPAs)

- Certified Public Accountant (CPA)

Over 25 years of experience and expertise in business valuations and appraisals. An accredited appraiser receives extensive training, remains in good standing, and follows specific industry practices to determine the value of a business.

GCF’s Machinery and Equipment Appraisal Accreditations

Expert Equipment Certified Appraiser (EECA) – Our appraisers are recognized with a deep understanding of valuation principles and extensive experience by the Institute of Equipment Valuation.

Expert Equipment Certified Appraiser (EECA) – Our appraisers are recognized with a deep understanding of valuation principles and extensive experience by the Institute of Equipment Valuation.

- Certified Machinery and Equipment Appraiser (CMEA) – a CMEA professional has the expertise and certification to conduct a third party machinery and equipment appraisal.

The GCF Business Valuation Process