The Great Debate: Business Valuations With Or Without Inventory

Steve Mize, ASA

In small business transactions, purchase agreements can be written any number of ways. For those businesses that are dependent on inventory to generate revenue and cash flow, you’ll typically see the purchase agreements structured where the Price includes Inventory or Price + Inventory.

All qualified appraisers agree that inventory is REQUIRED to generate cash flow and therefore the inventory should transfer with the new business as part of the final transaction price. The sticking issue is how to value a business when the purchase agreement states inventory is separate from the purchase price. An appraiser can value the business both ways, but MUST (1) calculate the value of the business correctly and (2) state whether or not inventory is or is not included in the value. It’s not just a matter of adding or subtracting, there is more to it and it starts with calculating the Income and Market Approaches accurately.

Example 1: Income Approach

Let’s say we’re engaged to value a liquor store WITHOUT inventory. Can we do this, yes…But the total value needs to be adjusted for a working capital deficit. For instance:

SDE – $160,000 (calculated as EBITDA + add-backs + officer salary)

Net Cash Flow = $100,000 (after tax, after working capital requirement, fair salary, etc)

Cap rate / WACC = 18% (normal build-up / public company stocks)

Inventory = $125,000

$100,000 / 18% = $555,556 (traditional capitalization of earnings approach)

Arriving at the cash flows above you need inventory valuation. The cap rate is based on other companies where inventory is included in the price (market cap). Therefore, the value of $555,556 INCLUDES inventory. So when the purchase price for the business is separate from inventory, our appraisers must make the following adjustment:

Total Value Including Inventory = $555,556

Less, Normal inventory of $125,000

Value of Business Without Inventory = $430,556

Example 2: Market Approach

Same scenario as above using “Bizcomps”, the only transaction database that does NOT include inventory in their transaction multiples. BizComps’ price to earnings multiples for liquor stores are much lower vs other databases because those multiples DO NOT include inventory. Example using Bizcomps:

SDE = $160,000

Bizcomps MEDIAN Average Liquor Store Multiplier = 2.6x

If a lender wants GCF to value the business WITHOUT inventory, there is no adjustment for a working capital deficit as inventory is NOT included in this method. The calculation is as follows:

SDE of $160,000 x median average multiple of 2.6x = $416,000

Example 3: Market Approach

Same scenario with a different transaction database. ALL databases except for Bizcomps include inventory in their price to earnings multiples unless the notes say otherwise. This includes DealStats, PeerComps, and IBA Database as the primary sources for small business transactions. For this example, we will use PeerComps. The Median SDE multiple for a liquor store in the PeerComps transaction database is 3.44x. The multiple is higher because it INCLUDES inventory. The value is calculated as follows:

SDE = $160,000 x 3.44 = $550,400.

If the lender wants GCF to value the business WITHOUT inventory, we then subtract inventory. That calculation is as follows:

Value of $550,400

Less Inventory of $125,000

Value Without Inventory of $425,400

With all 3 examples above, we have properly accounted for the variables that influence the value of the business and then calculated the business WITH and WITHOUT inventory. We’ve seen accredited appraisers calculate the Market Approach using transaction data that already includes inventory and then add inventory on top of that. We’ve also seen accredited appraisers calculate the Income Approach using cap rates that include normal working capital yet forget to deduct the inventory from their calculation when the price doesn’t include inventory. Just because your appraiser is accredited doesn’t mean they won’t make critical mistakes like this. Always Ask Questions!

For these kinds of situations, anyone from GCF can help to review another report and make sure the proper calculations are being made.

If you’re ever unsure, just call us at (813) 258-1668 or email us at connect@gvalue.com.

Reach out to GCF Valuation to discuss anything transaction or valuation related.

Questions about valuing your business? Please contact us with the button below, and a GCF appraiser will get in touch with you directly.

Keep learning about Business Valuations

– Why & When You Need a Business Valuation

– Different Types of Business Valuations

Business Valuation Accreditation

Your GCF Business Valuation appraisal team has one or more of the following business valuation accreditations:

Accredited Senior Appraiser (ASA) – is recognized as having achieved the highest level of education, training, and report writing for business valuations. The ASA designation is the gold standard for a business valuation professional. (source: American Society of Appraisers)

Accredited Senior Appraiser (ASA) – is recognized as having achieved the highest level of education, training, and report writing for business valuations. The ASA designation is the gold standard for a business valuation professional. (source: American Society of Appraisers)

Certified Business Appraiser (CBA) – a very prestigious credential in the eyes of all who are familiar with it as it earned the reputation of being a difficult credential to obtain. (source: National Association of Certified Valuators and Analysts®)

Certified Business Appraiser (CBA) – a very prestigious credential in the eyes of all who are familiar with it as it earned the reputation of being a difficult credential to obtain. (source: National Association of Certified Valuators and Analysts®)

Certified Valuation Analyst (CVA)

Certified Valuation Analyst (CVA) Accredited in Business Valuation by the American Institute of CPAs (ABV by AICPA) – a credential granted exclusively by the AICPA to qualified valuation professionals who demonstrate expertise in valuation through knowledge, skill, experience, and adherence to professional standards. (source: American Institute of CPAs)

Accredited in Business Valuation by the American Institute of CPAs (ABV by AICPA) – a credential granted exclusively by the AICPA to qualified valuation professionals who demonstrate expertise in valuation through knowledge, skill, experience, and adherence to professional standards. (source: American Institute of CPAs)

- Accredited in Business Valuation (ABV) – credential is granted exclusively by the AICPA to CPAs and qualified valuation professionals who demonstrate considerable expertise in valuation through their knowledge, skill, experience, and adherence to professional standards. (source: American Institute of CPAs)

- Certified Public Accountant (CPA)

Over 25 years of experience and expertise in business valuations and appraisals. An accredited appraiser receives extensive training, remains in good standing, and follows specific industry practices to determine the value of a business.

GCF’s Machinery and Equipment Appraisal Accreditations

Expert Equipment Certified Appraiser (EECA) – Our appraisers are recognized with a deep understanding of valuation principles and extensive experience by the Institute of Equipment Valuation.

Expert Equipment Certified Appraiser (EECA) – Our appraisers are recognized with a deep understanding of valuation principles and extensive experience by the Institute of Equipment Valuation.

- Certified Machinery and Equipment Appraiser (CMEA) – a CMEA professional has the expertise and certification to conduct a third party machinery and equipment appraisal.

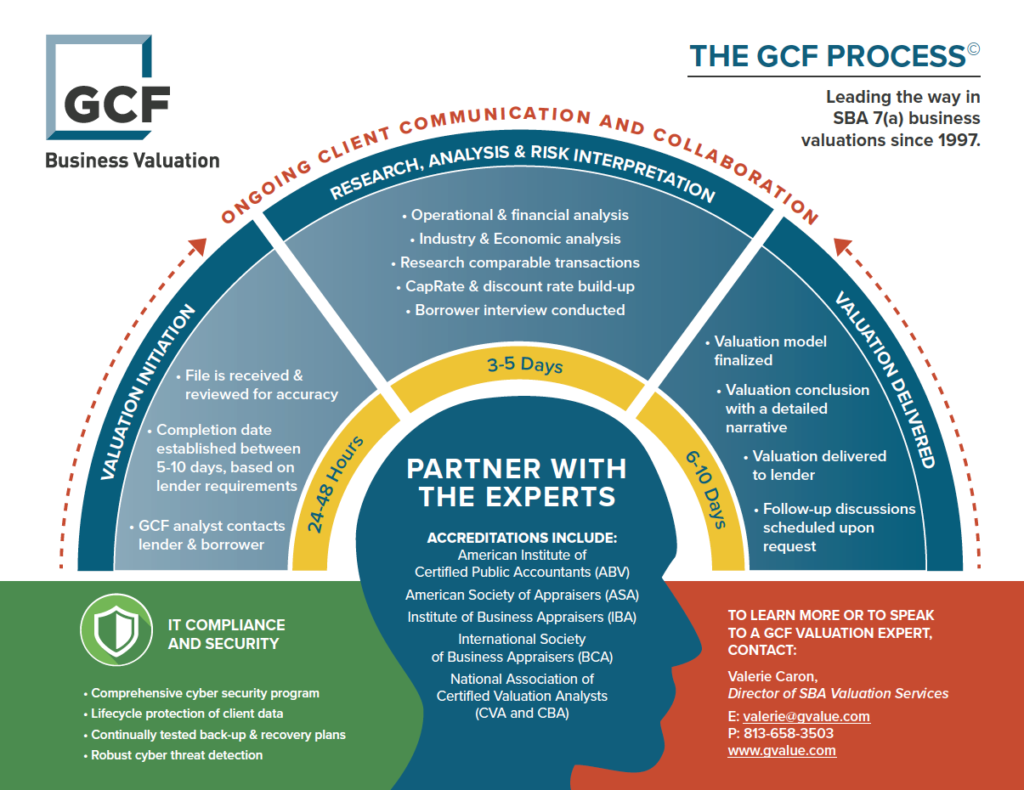

The GCF Business Valuation Process