Professional Equipment Appraisals: A Complete Guide for Lenders and Owners

Equipment Appraisal: A Complete Guide to Accurate Equipment Valuations

When equipment underpins your operations, treating its value as an afterthought can derail loans, deals, and planning. A professional Machinery & Equipment (M&E) Appraisal gives lenders, buyers, and owners a defensible, well-documented view of what their machinery and equipment are truly worth. If equipment collateral cannot be clearly supported, the deal does not move forward, regardless of borrower strength.

For a rigorous, SBA‑compliant opinion of value on your equipment, you can visit GCF’s equipment appraisal page to get started.

What Is Equipment Appraisal and Why It Matters

An M&E Appraisal is an independent, professional opinion of value on tangible assets such as equipment, vehicles, production lines, and other fixed assets. Instead of relying on book value or informal dealer quotes, an equipment appraisal uses market data, recognized valuation methods, and clearly documented assumptions to arrive at a supportable conclusion. This is not a valuation exercise; it’s a credit decision tool.

An M&E Appraisal is a critical component of equipment valuation because it directly affects financing decisions, insurance coverage, tax reporting, and transaction pricing.

When Do You Need an Equipment Appraisal?

You should consider an M&E Appraisal any time a major decision or transaction hinges on the value of your equipment and tangible assets.

Financing and SBA or Conventional Lending

Lenders regularly rely on equipment collateral to support collateral-based term loans, SBA 7(a) and 504 financing, and asset-based lending vehicles. SBA guidance pushes lenders toward independent M&E Appraisals when equipment is a key piece of the collateral package, rather than relying solely on book values.

When a borrower’s balance sheet includes substantial equipment—whether in construction, transportation, manufacturing, or healthcare—an SBA‑compliant, audit-ready M&E Appraisal from GCF helps lenders justify loan amounts, advance rates, and collateral coverage to credit committees and examiners.

Buying or Selling a Business With Significant Equipment

In many industries, equipment drives a large share of business value. Buyers and sellers in sectors like construction, transportation and warehousing, manufacturing, and even service businesses with specialized tools all need a clear view of fair market value for equipment to negotiate effectively.

Business Valuation for Construction highlights how dependence on equipment and tangible assets complicates valuation for contractors, underscoring the need for accurate equipment values within broader business appraisals.

Insurance, Tax, and Financial Reporting

Insurance carriers and tax authorities expect defensible numbers. An M&E Appraisal provides a more accurate basis for setting insurable value, handling property tax assessments, and supporting depreciation and impairment testing than outdated cost records or generic schedules.

Accurate equipment values also feed into broader business valuation work and market intelligence. For example, GCF’s Market Intelligence reports on industries like construction contractors, automotive repair, or convenience stores offer context on how tangible assets and capital expenditures impact overall value.

Legal Disputes, Divorce, and Buyouts

In disputes, divorces, and partner buyouts, opposing sides frequently disagree on what equipment is worth. A neutral, third‑party M&E Appraisal provides an objective benchmark that attorneys, mediators, and courts can rely on when dividing assets or calculating damages.

Because GCF’s appraisers hold designations like Expert Equipment Certified Appraiser (EECA) and Certified Machinery and Equipment Appraiser (CMEA), our reports carry credibility in contentious settings.

Types of Equipment Appraisals: On‑Site vs Desktop

Different situations call for different appraisal formats. GCF offers both inspection-based and desktop equipment appraisals to match the risk and purpose of each engagement.

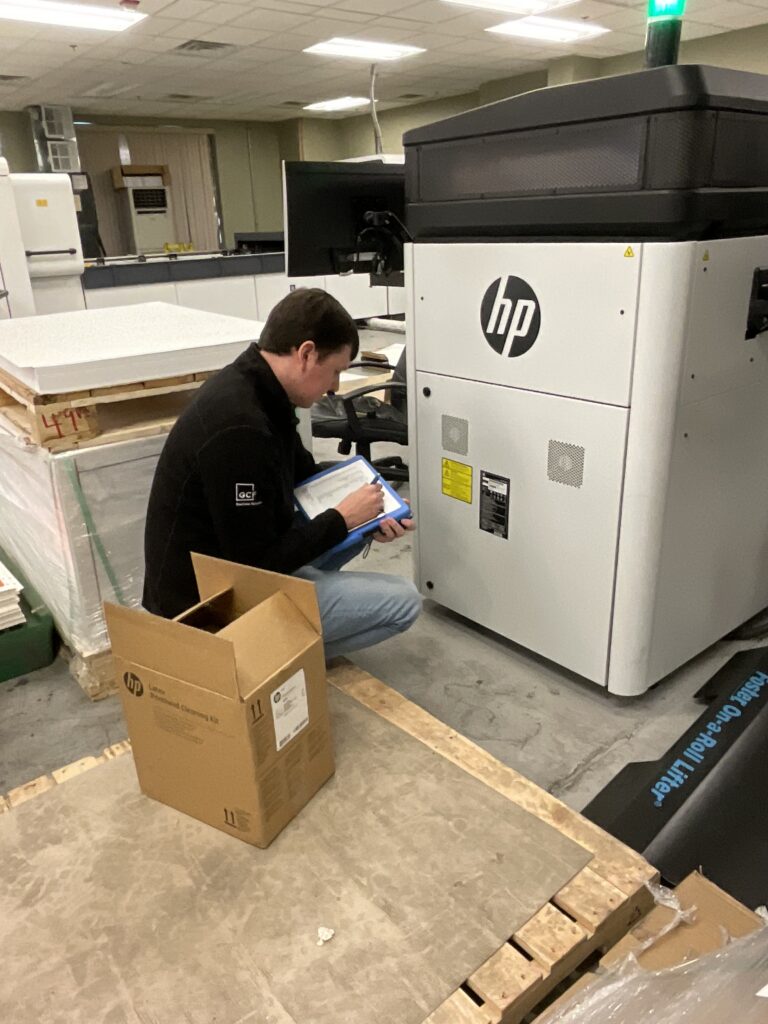

On‑Site Equipment Appraisal

In an on‑site equipment appraisal, an appraiser visits your location to physically inspect the equipment. They verify that each asset exists, confirm make, model, and serial numbers, observe condition and functionality, and document the equipment with photos.

For SBA lending, bank exams, and higher‑risk or high‑dollar exposures, on‑site equipment appraisals are often preferred because condition, maintenance, and usage materially impact value. GCF performs these inspections with in‑house accredited appraisers, and they are designed to stand up to any audit.

Desktop (Document‑Based) Equipment Appraisal

Desktop equipment appraisals are completed remotely, using asset lists, photos, maintenance records, and other documents provided by the client, without a physical inspection. The same valuation principles apply, but the appraiser must rely on the completeness and accuracy of the provided data.

This format can work well for internal planning, lower‑risk collateral checks, or standardized equipment across multiple sites.

How Equipment Appraisers Determine Value

Equipment Appraisal: Understanding the Process lays out a clear, step‑by‑step framework.

Step 1: Scoping the Engagement

The process starts with a conversation about purpose, intended use, and key assumptions:

- What decision is this appraisal supporting (loan, sale, dispute, planning)?

- Which equipment is in scope, and what standard of value is required (fair market value, orderly liquidation value, forced liquidation value)?

- Are there regulatory or SBA requirements to meet?

Step 2: Inspection and Data Collection

Next comes gathering detailed equipment information. For on‑site work, which includes physical inspection. For desktop work, it involves more intensive documentation gathering.

Typical data points include:

- Make, model, year, and serial number

- Capacity and technical specifications

- Operating hours, mileage, or usage metrics

- Maintenance and repair history

- Prior upgrades or retrofits

Step 3: Market Research and Valuation Approaches

Once data is in hand, the appraiser researches market conditions and applies the three core approaches to value:

- Cost approach: Estimate current replacement cost and adjust for age, condition, and obsolescence.

- Market (sales comparison) approach: Compare to recent sales or listings of similar equipment, adjusted for specs and condition.

- Income approach: When appropriate, tie value to cash flows or cost savings attributable to the equipment.

Each approach has strengths depending on the asset type and data available. For common, actively traded equipment, the market approach often carries the most weight. For specialized or newer assets, the cost approach may be more informative. In rare cases where an asset directly generates distinct revenue, the income approach can provide another lens.

Step 4: Analysis, Reconciliation, and Reporting

Finally, the appraiser reconciles indications from each approach to conclude value, then prepares a written report that documents:

- Scope of work and purpose

- Data sources and assumptions

- Methods used and why

- Final value conclusions (by asset and/or in aggregate)

Information to Prepare Before Ordering an Equipment Appraisal

You can speed up an M&E Appraisal and improve accuracy by gathering key information in advance.

- Detailed equipment list with description, make, model, year, and serial number

- Location of each asset, including multiple sites if applicable

- Usage metrics (hours, mileage, cycles, etc.)

- Maintenance and repair records

- Purchase invoices and documentation for major upgrades or retrofits

- Photos showing general condition, control panels, and nameplates

Read our blog, Equipment Appraisal: Understanding the Process, here.

🚩Common Mistakes That Hurt Equipment Appraisal Results 🚩

- Relying on book value alone. Tax and accounting values often diverge significantly from market reality, especially for older or heavily used equipment.

- Incomplete or inaccurate equipment lists. Missing serial numbers, vague descriptions, or omitted assets lead to conservative assumptions and weaker collateral support.

- Poor maintenance and documentation. Lack of service records or visible neglect harms both actual value and appraiser confidence.

- Choosing a non‑specialist appraiser. Without dedicated equipment experience and certifications like EECA or CMEA, reports may not hold up with lenders or in disputes.

How to Choose the Right Equipment Appraisal Partner

Not all valuation providers are created equal. For complex transactions, SBA lending, or litigation, you need a firm with both depth and specialization.

When evaluating an M&E Appraisal partner, look for:

- Specialized certifications. Designations like Expert Equipment Certified Appraiser (EECA) and Certified Machinery and Equipment Appraiser (CMEA) indicate focused expertise.

- SBA and lender experience. A provider known among SBA lenders and banks for reports that survive underwriting and exams is especially valuable when equipment is key collateral.

- National reach and capacity. If your portfolio spans multiple states or industries, you need a team that can handle varied equipment types and geographies without sacrificing quality or speed.

- Clear process and realistic timelines. A typical turnaround of about 10–12 business days after receiving all data and completing inspections for M&E assignments, giving clients predictable schedules.

- No Outside Contractors. For the best results, the firm you select should employ the M&E Appraiser doing the work.

Traditional Meets Data-Driven: The Modern Business Broker’s Guide to Valuations

Connecting Equipment Appraisal With Broader Valuation and Market Insight

One advantage of working with a full‑service valuation firm is the ability to connect equipment values with broader business and industry context.

GCF’s Insights platform combines:

Ready for a Professional Equipment Appraisal?

Whether you are an SBA lender evaluating collateral, a business owner preparing for a sale, or an advisor guiding clients through complex transactions, relying on guesswork for equipment values is no longer enough. A thorough, SBA‑compliant M&E Appraisal from GCF gives you a clear, defensible opinion of value backed by experienced, accredited appraisers and a proven process.

To explore options, timelines, and pricing for your next assignment, visit GCF’s equipment appraisals page and connect with their dedicated team.

Keep Learning About Business Valuations

How to Navigate The Business Valuation Process Successfully

The Great Debate: Business Valuation With or Without Inventory

What Is Business Valuation? Why & When You Need One

Our Accreditations

Your GCF Business Valuation appraisal team has one or more of the following business valuation accreditations:

![]() Accredited Senior Appraiser (ASA) – is recognized as having achieved the highest level of education, training, and report writing for business valuations. The ASA designation is the gold standard for a business valuation professional. (source: American Society of Appraisers)

Accredited Senior Appraiser (ASA) – is recognized as having achieved the highest level of education, training, and report writing for business valuations. The ASA designation is the gold standard for a business valuation professional. (source: American Society of Appraisers)

Certified Business Appraiser (CBA) – a very prestigious credential in the eyes of all who are familiar with it as it earned the reputation of being a difficult credential to obtain. (source: National Association of Certified Valuators and Analysts®)

Certified Valuation Analyst (CVA)

Certified Valuation Analyst (CVA)

![]() Accredited in Business Valuation by the American Institute of CPAs (ABV by AICPA) – a credential granted exclusively by the AICPA to qualified valuation professionals who demonstrate expertise in valuation through knowledge, skill, experience, and adherence to professional standards. (source: American Institute of CPAs)

Accredited in Business Valuation by the American Institute of CPAs (ABV by AICPA) – a credential granted exclusively by the AICPA to qualified valuation professionals who demonstrate expertise in valuation through knowledge, skill, experience, and adherence to professional standards. (source: American Institute of CPAs)

Accredited in Business Valuation (ABV) – credential is granted exclusively by the AICPA to CPAs and qualified valuation professionals who demonstrate considerable expertise in valuation through their knowledge, skill, experience, and adherence to professional standards. (source: American Institute of CPAs)

- Certified Public Accountant (CPA)

Over 25 years of experience and expertise in business valuations and appraisals. An accredited appraiser receives extensive training, remains in good standing, and follows specific industry practices to determine the value of a business.

GCF’s Machinery and Equipment Appraisal Accreditations

Expert Equipment Certified Appraiser (EECA) – Our appraisers are recognized with a deep understanding of valuation principles and extensive experience by the Institute of Equipment Valuation.

Expert Equipment Certified Appraiser (EECA) – Our appraisers are recognized with a deep understanding of valuation principles and extensive experience by the Institute of Equipment Valuation.

- Certified Machinery and Equipment Appraiser (CMEA) – a CMEA professional has the expertise and certification to conduct a third party machinery and equipment appraisal.